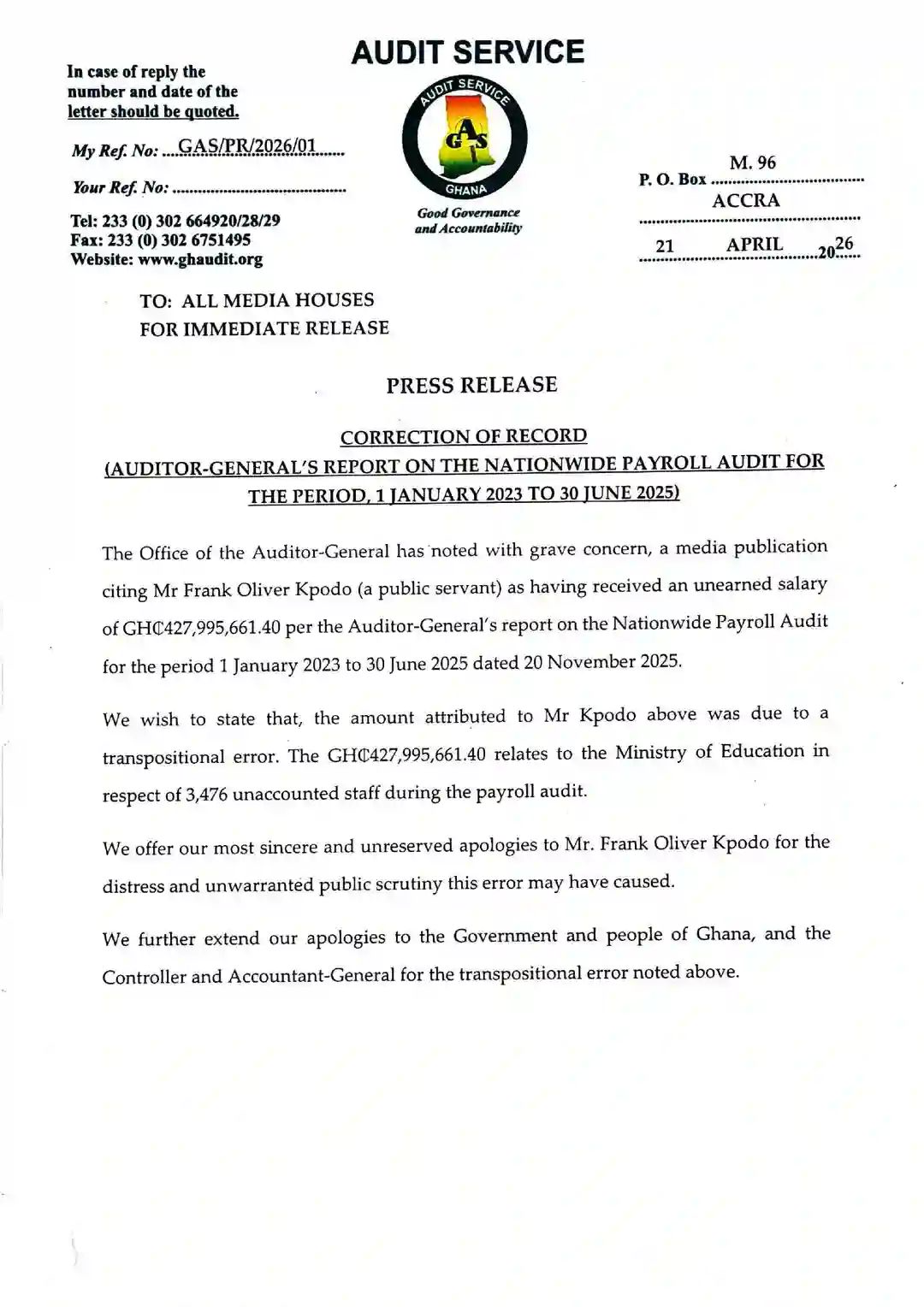

The public audit system is under scrutiny after a payroll audit error wrongly linked GH¢427.9 million in unearned salary payments to an individual, before later correcting the figure. The Audit Service of Ghana said the amount, initially associated with Frank Oliver Kpodo in media reports, was the result of a “transpositional error” in its nationwide payroll audit covering January 2023 to June 2025. In a statement dated April 21, the Office of the Auditor-General of Ghana clarified that the GH¢427.9 million figure relates instead to the Ministry of Education, covering 3,476 unaccounted staff identified during the audit. “We offer our most sincere and unreserved apologies to Mr. Frank Oliver Kpodo for the distress and unwarranted public scrutiny this error may have caused,” the office said, adding apologies to the government, the public and the Controller and Accountant-General’s Department. While the correction resolves the misattribution, the scale of the error triggers concerns about the reliability of public financial oversight systems at a time of heightened scrutiny over fiscal discipline. Audit reports issued by the Auditor-General are central to public accountability and are widely used by policymakers, development partners and investors to assess governance risks and expenditure controls. A misstatement involving a figure of this magnitude raises questions about data verification and quality control processes within the audit system. The incident risks undermining confidence in official financial reporting, particularly as Ghana seeks to strengthen credibility around public sector reforms and fiscal consolidation efforts. READ ALSO When the Cash Cows Get Leaner: Receipts from Cocoa & Crude Record Huge Decline in First 2 Months of 2026 Priced Out of Paradise: Are Ghana’s Hotel Rates Undermining Its Tourism Ambitions? Towards a Seamless & Cheaper Remittance Inflows: How the BoG is Working to Remove Bottlenecks Beyond institutional credibility, the error poses potential reputational and legal risks associated with public financial reporting. Wrongly attributing such an amount in alleged irregular payments to an individual carries consequences that may extend beyond a later correction. Even where errors are unintentional, such disclosures can trigger public backlash, reputational damage and potential legal claims, underscoring the sensitivity of audit communication. Despite the correction, the underlying findings of the audit remain significant, pointing to thousands of unaccounted staff within the education sector alone. These discrepancies reinforce long-standing concerns over payroll management in the public sector, where governments continue to pursue reforms aimed at reducing inefficiencies and eliminating ghost workers. Statement Below; Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Like this:Like Loading... Related

politics

Auditor-General Corrects Payroll Audit Error After Misattributing GH¢428 Million

The High Street JournalBy Isaac Kofi TsoenamawuTue, 21 Apr 2026 · 1h ago0 views

Share:

Photo credit: The High Street Journal

The Auditor-General of Ghana corrected a payroll audit error, retracting the misattribution of GH¢427.9 million in unearned salary payments to an individual. The office stated the figure, initially linked to Frank Oliver Kpodo, was a "transpositional error." The amount actually pertains to the Ministry of Education, involving 3,476 unaccounted staff. The Auditor-General apologized for the error and distress caused.

Source

The High Street Journal

#["Business & Economy"#"Auditor-General"#"Mr. Frank Oliver Kpodo"#"Payroll Audit"]